NAEPC Webinars (See All):

Issue 44 – July, 2024

Application of the Corporate Transparency Act to Common Trust Structures

By Christina S. Hammervold, JD

Under the Corporate Transparency Act (the “CTA”), limited liability companies, corporations and other business entities generally must disclose information about their beneficial owners to the Financial Crimes Enforcement Network—otherwise known as FinCEN. Although FinCEN has issued regulations on how to determine an entity’s beneficial owners, determining an entity’s beneficial owners can be challenging when the entity is owned directly or indirectly by a trust. This article explores several examples of how the CTA may apply when a reporting company is owned by a trust and highlights unanswered questions about how the CTA should be applied to certain trust structures.

Under the Corporate Transparency Act (CTA), limited liability companies (LLCs), corporations and other business entities are required to disclose information about their beneficial owners to the Financial Crimes Enforcement Network (FinCEN),[1] unless they qualify for an exemption.[2] FinCEN has issued regulations detailing which beneficial owners must file a beneficial ownership information report, how to determine an entity’s beneficial owners, what information has to be reported for the entity and its beneficial owners,[3] and when a report must be filed.[4] When an entity is owned and controlled by individuals, it is generally a simple process to determine the entity’s beneficial owners. However, determining an entity’s beneficial owners can be challenging when the entity is owned directly or indirectly by a trust. This article explores a few common trust structures to illustrate how the CTA applies when a reporting company is owned by a trust. As highlighted below, there are many unresolved issues and questions on how the CTA should be applied to trust structures.

Brief Background on the CTA

Reporting Companies. The CTA, which took effect on January 1, 2024, imposes filing requirements on reporting companies, which include domestic reporting companies and foreign reporting companies.[5] Generally, domestic reporting companies include corporations, LLCs, and other entities created by filing a document with a secretary of state or any similar office under the law of a U.S. state or American Indian tribe.[6] Foreign reporting companies include non-U.S. corporations, non-U.S. LLCs, and other non-U.S. entities that are registered to do business in the U.S. by the filing of a document with a secretary of state or any similar office under the law of a U.S. state or American Indian tribe.[7] Importantly, many trusts for estate planning purposes do not qualify as reporting companies because such trusts generally are not created (or registered to do business) by the filing of a document with a secretary of state or similar office.[8] The CTA provides 23 categories of exemptions, and the exemptions generally cover highly-regulated entities and other “low-risk” entities (e.g., large operating companies with a physical presence in the U.S., 501(c) nonprofit organizations, charitable trusts, split-interest trusts, publicly traded companies, SEC-registered companies, insurance companies, banks, etc.).[9] Most privately-held entities used for estate planning, investment, real estate, tax, privacy, or other personal planning generally will not be exempt.

Beneficial Owners. Under the CTA, reporting companies are required to report their beneficial owners to FinCEN. Generally, the term “beneficial owner” is defined broadly to include any individual who, directly or indirectly:

- Exercises substantial control over the entity (the substantial control test), or

- Owns or controls at least 25% of the ownership interests of the entity (the ownership test).[10]

For this purpose, “substantial control” includes:

- Service as a senior officer;

- Authority to appoint or remove a senior officer or a majority of the board (or similar body);

- Directing, determining, or having substantial influence over important company decisions; or

- Any other form of substantial control.[11]

FinCEN has emphasized that “[e]xercising substantial control or owning or controlling ownership interests may be direct or indirect, including through any contract, arrangement, understanding, relationship, or otherwise.”[12]

Importantly, a beneficial owner must be an individual.[13] This means that when an entity holds substantial control over or ownership of a reporting company, the reporting company must generally look through the secondary entity with substantial control/ownership to determine the individual beneficial owners of the reporting company. Certain individuals are excluded from the definition of beneficial owner, including a minor (provided the reporting company reports the required information of a parent or legal guardian of the minor) and an individual acting as a nominee, intermediary, custodian, or agent on behalf of another individual.[14]

Further, the obligation to disclose current beneficial ownership is an ongoing requirement. Reporting companies are required to file updated beneficial ownership information reports when there are any changes to their beneficial ownership (or any change with respect to the information reported for the reporting company or a beneficial owner, such as a change of address).[15]

To understand how the CTA works in practice, it is helpful to explore a few common ownership structures.

Determining Beneficial Ownership for Common Structures

The following examples explore how to determine the beneficial owners of a reporting company for CTA purposes, starting with a simple structure and then exploring more complex structures. It must be noted that determining beneficial ownership is a fact-specific exercise. The examples below are provided to illustrate CTA concepts and open issues, and should not be construed as legal advice or as an opinion on specific situations. If you have a question regarding how to determine beneficial ownership of a reporting company under the CTA, or whether the CTA applies to an entity, please consult with your legal advisor.

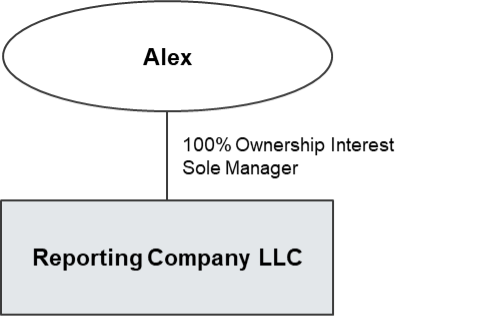

Example 1 – Reporting Company LLC. The following is an example of a simple structure:

In this example, “Alex” is the sole beneficial owner of Reporting Company LLC because he is a beneficial owner under both the substantial control and ownership tests. Here, Alex is the sole manager of Reporting Company LLC, and he owns all of the voting rights of the LLC. Also, in our example, no other person holds any powers with respect to Reporting Company LLC that could be considered “substantial control” (e.g., there are no officers of Reporting Company LLC). Alex is, therefore, the sole beneficial owner under the substantial control test. Alex is also the sole owner of Reporting Company LLC and no other person owns or controls any ownership interest in Reporting Company LLC. Thus, Alex is also the sole beneficial owner under the ownership test.

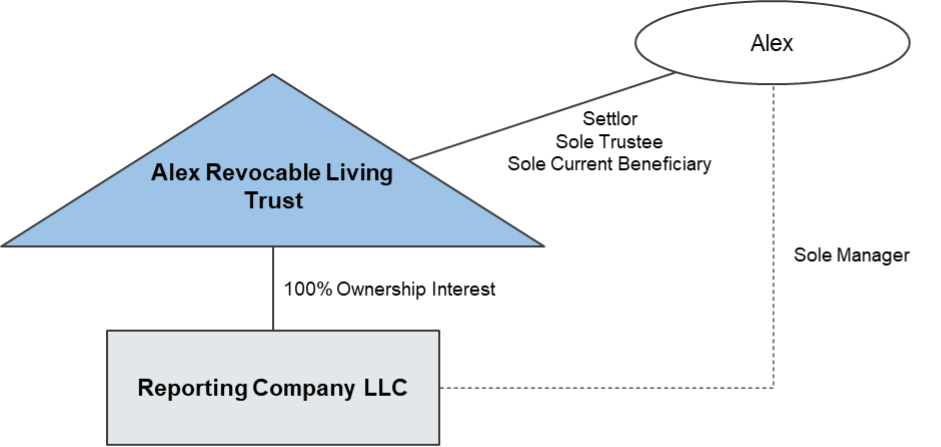

Example 2 – Revocable Living Trust. Below is an example of a revocable living trust structure:

In this example, Alex should be the sole beneficial owner of Reporting Company LLC, but the CTA analysis is more involved. First, during Alex’s lifetime, he should be considered the sole beneficial owner under the substantial control test because he is: (1) the sole manager of Reporting Company LLC, and (2) the sole controlling person of the Alex Revocable Living Trust (which is the sole owner of Reporting Company LLC).[16] Second, during Alex’s lifetime, he should be considered the sole beneficial owner under the ownership test because he is the only individual who has a current control position or current beneficial interest in the Alex Revocable Living Trust (which is the sole owner of Reporting Company LLC).

In this example, because Reporting Company LLC is owned by a trust, rather than by an individual, we must look through the trust to determine the beneficial owners of the LLC to be reported under the CTA. Under the CTA, if an ownership interest in a reporting company is held by the trustee of a trust, each of the individuals below are deemed to have an ownership interest in the reporting company:

- A settlor who has the right to revoke the trust or otherwise withdraw the trust’s assets;

- A beneficiary who is the sole permissible recipient of the trust’s income and/or principal;

- A beneficiary who has the right to demand a distribution of, or withdraw substantially, all of the trust’s assets;

- A trustee of the trust;[17] or

- Any other individual who has the “authority to dispose of trust assets.”[18]

Depending on the specific circumstances, other individuals may also be considered to own or control ownership interests held by the trustee of a trust (e.g., trust protectors of a trust, distribution or investment advisors of a trust, or discretionary beneficiaries of a trust with multiple beneficiaries).[19] In addition, depending on the trust instrument, the ownership interests held by the trustee of a trust could be considered as simultaneously owned or controlled by multiple individuals of a trust.[20]

In this Example 2, during Alex’s lifetime:

- Alex (as settlor) has the right to revoke the Alex Revocable Living Trust.

- Alex is the only permissible recipient of the Alex Revocable Living Trust’s income and/or principal.

- Alex is the sole trustee of the Alex Revocable Living Trust.

- No other individual has the authority to dispose of the assets of the Alex Revocable Living Trust.

- Other than Alex, there are no other individuals that hold power over or have current beneficial interests in the Alex Revocable Living Trust (e.g., there is no distribution advisor, no investment advisor, no trust protector, and no other current beneficiaries).

Under these facts, during Alex’s lifetime he should be the only beneficial owner of Reporting Company LLC. Upon Alex’s death, however, a change of beneficial ownership will occur and Reporting Company LLC will have to timely file an updated beneficial ownership information report with FinCEN.[21]

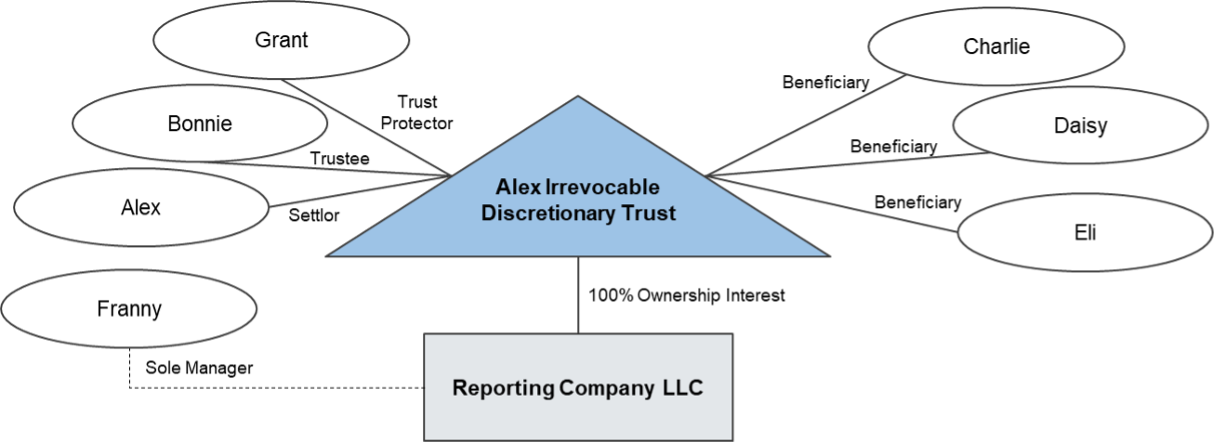

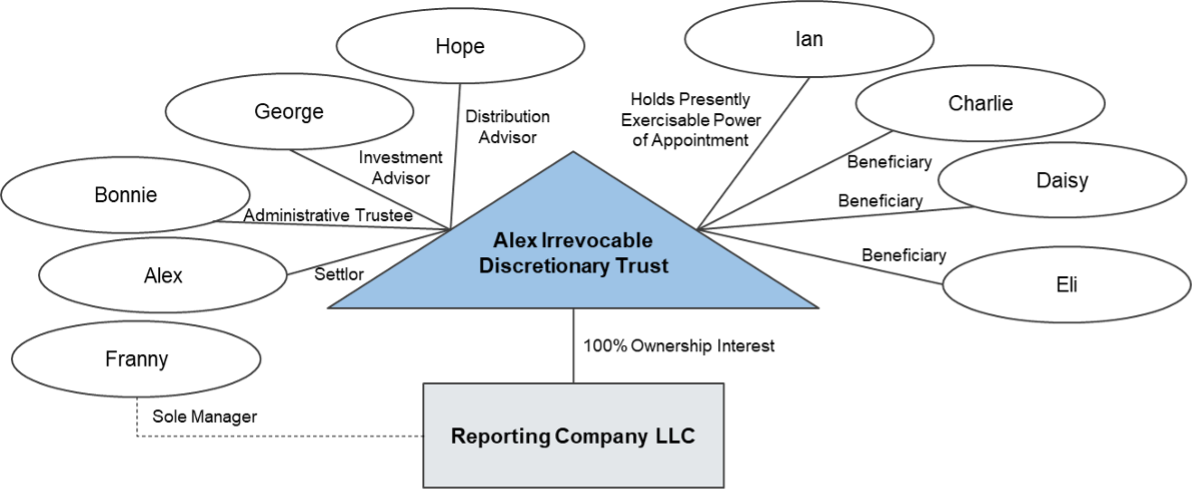

Example 3 – Irrevocable Discretionary Trust with Multiple Beneficiaries. Next is an example of an irrevocable discretionary trust with multiple beneficiaries:

Unfortunately, the available CTA rules and guidance do not clearly articulate how to determine the beneficial owners under this Example 3. While the guidance is fairly clear that Franny (as the sole manager of Reporting Company LLC) and Bonnie (as the trustee of the Alex Irrevocable Discretionary Trust) should be considered beneficial owners of Reporting Company LLC, the breadth and ambiguity of the regulations make it unclear whether any other individuals could be considered beneficial owners of Reporting Company LLC.

Reporting Company LLC may desire to take the position that (1) Alex (the settlor) is not a beneficial owner of Reporting Company LLC because he does not have the power to revoke the trust or otherwise withdraw the trust’s assets; and (2) Charlie, Daisy, and Eli (the discretionary beneficiaries) are not beneficial owners of Reporting Company LLC because they are each only discretionary beneficiaries of a trust with multiple beneficiaries and none of them have the power to demand a distribution of, or withdraw substantially all of, the trust’s assets.

Although these positions may be possible given the plain language of the CTA regulations, FinCEN has made clear that the specified categories listed in the CTA regulations are merely examples and do not address all applications under which individuals may be considered to own or control ownership interests through a trust.[22] Thus, it is possible that a settlor or beneficiary may be considered a beneficial owner for CTA purposes, even if they fall outside one of the specified categories in the CTA regulations. Additionally, because of the breadth of the definitions of substantial control and ownership interest, other roles within a trust arrangement may be reportable, such as trust protectors, distribution advisors, or investment advisors (as further discussed below).

Returning to this Example 3, Reporting Company LLC may be required to report Alex, Charlie, Daisy, and/or Eli as beneficial owners, depending on the specific circumstances. Currently, there appear to be at least three approaches as to whether to report beneficiaries of a discretionary spray trust:

- Do not report any beneficiary (so long as there is more than one current beneficiary),

- Report all living discretionary beneficiaries, or

- Adopt a facts-and-circumstances approach to determine whether to report a particular discretionary beneficiary.

Under the current regulations and guidance, Reporting Company LLC may be able to reasonably take the approach that it is not required to report Charlie, Daisy, or Eli. However, because FinCEN has specifically stated that the reportable trust categories are illustrative—and not exhaustive—it is possible that FinCEN could later challenge this approach, depending on the particulars of the case. The most conservative approach would be for Reporting Company LLC to report each of Charlie, Daisy, and Eli as the living discretionary beneficiaries of the Alex Irrevocable Discretionary Trust. While this approach is arguably not required by the CTA rules, some practitioners recommend this conservative approach due to the ambiguity of the current rules and guidance. Finally, Reporting Company LLC could adopt a facts-and-circumstances approach to decide whether to report a particular discretionary beneficiary, which could result in the disclosure of some (but not all) beneficiaries.

Finally, assume that Grant (as the trust protector of the trust) has the power to replace a trustee. As stated above, substantial control includes the power to appoint or remove a senior officer or a majority of the board (or similar body) of a reporting company. Here, Grant’s power is one step removed—he has the power to replace the trustee of the Alex Irrevocable Discretionary Trust, who in turn has the power to replace the manager of Reporting Company LLC. While the regulations are clear that substantial control can be indirect,[23] one may reasonably argue that Grant’s power to replace the trustee is too tenuous to amount to substantial control over Reporting Company LLC. Indeed, while the manager of Reporting Company LLC has an active role in the management of Reporting Company LLC, the trustee of the Alex Irrevocable Discretionary Trust merely holds the beneficial ownership interest of the LLC on behalf of the discretionary beneficiaries and has no active role in management of the business. Thus, it appears unlikely that Grant has substantial influence over important LLC decisions or any other power that could be reasonably considered substantial control. Reporting Company LLC may be able to reasonably take the position that Grant (who only has the right to replace the trustee) should not be a beneficial owner of Reporting Company LLC. This position is far from definitive. Many advisors hope that FinCEN will issue guidance to resolve this uncertainty.

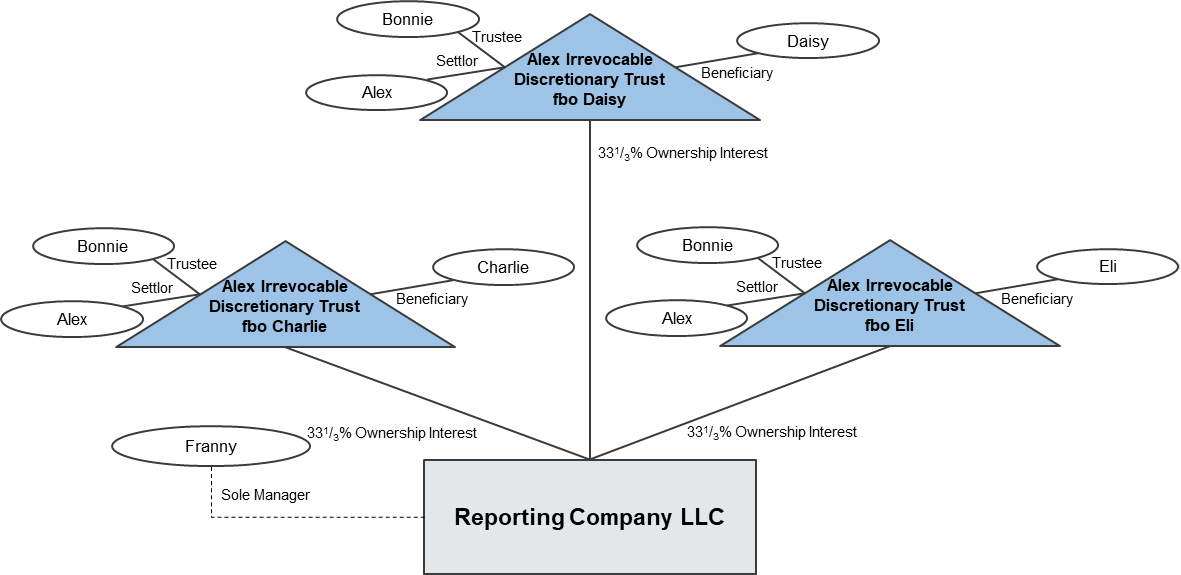

Example 4 – Irrevocable Trust Split into Separate Shares. In this Example 4, the Alex Irrevocable Discretionary Trust has divided into separate shares for each beneficiary, with Charlie, Daisy, and Eli each being the sole current permissible beneficiary of such person’s separate trust share. Assume that all other facts remain the same as under Example 3 above.

Where a separate share has only one current permissible beneficiary, it is generally prudent to treat that beneficiary as a beneficial owner for CTA purposes (assuming the separate share owns at least 25% of the reporting company, whether directly or indirectly). Thus, in this example, the prudent approach would be to report Charlie, Daisy, and Eli as beneficial owners of Reporting Company LLC because each of them is deemed to own 33.33% as a beneficiary of such person’s separate trust share.

Example 5 – Directed Trust. Here, the irrevocable discretionary trust is a directed trust with the following power holders and current beneficiaries:

In this example, George and Hope have the power to dispose of the Alex Irrevocable Discretionary Trust’s interest in Reporting Company LLC—George has the power (as investment advisor) to sell, liquidate, or otherwise dispose of Reporting Company LLC; and Hope has the power (as distribution advisor) to distribute ownership interests in Reporting Company LLC to one or more of the beneficiaries. Because George and Hope have the ability to “dispose of trust assets,” under the plain language of the CTA regulations, they should be deemed to each own the ownership interest in Reporting Company LLC held by the Alex Irrevocable Discretionary Trust (i.e., George and Hope each own 100% of Reporting Company LLC). Notably, similar reasoning should apply to an individual who holds a presently exercisable power of appointment that allows such individual to appoint trust property to a beneficiary. Therefore, George, Hope and Ian should each be considered beneficial owners of Reporting Company LLC.

We will assume here that Bonnie (as the administrative trustee of the trust) holds legal title to Reporting Company LLC on behalf of the discretionary beneficiaries of the trust, but that she cannot dispose of trust assets without an instruction from George (as the investment advisor of the trust) or Hope (as the distribution advisor of the trust). In such a directed trust context, we can reasonably debate whether Bonnie should be considered a beneficial owner under the CTA guidance, given her lack of authority over Reporting Company LLC. While the plain language of the CTA regulations arguably weighs in favor of reporting all trustees (including a directed trustee that does not have discretion to dispose of the reporting company), there is a potential argument that a directed trustee is merely acting as a nominee or agent and, therefore, should not be considered a beneficial owner because nominees and agents are excluded from the definition of beneficial owner under the CTA.[24] Additionally, in its frequently asked questions, FinCEN has arguably raised the possibility that some trustees may not be considered beneficial owners – “[p]articular facts and circumstances determine whether specific trustees, beneficiaries, grantors, settlors, and other individuals with roles in a particular trust are beneficial owners of a reporting company whose ownership interests are held through that trust.”[25] Of course, the conservative position is to report Bonnie as a beneficial owner of Reporting Company LLC, particularly given her legal ownership of Reporting Company LLC.[26]

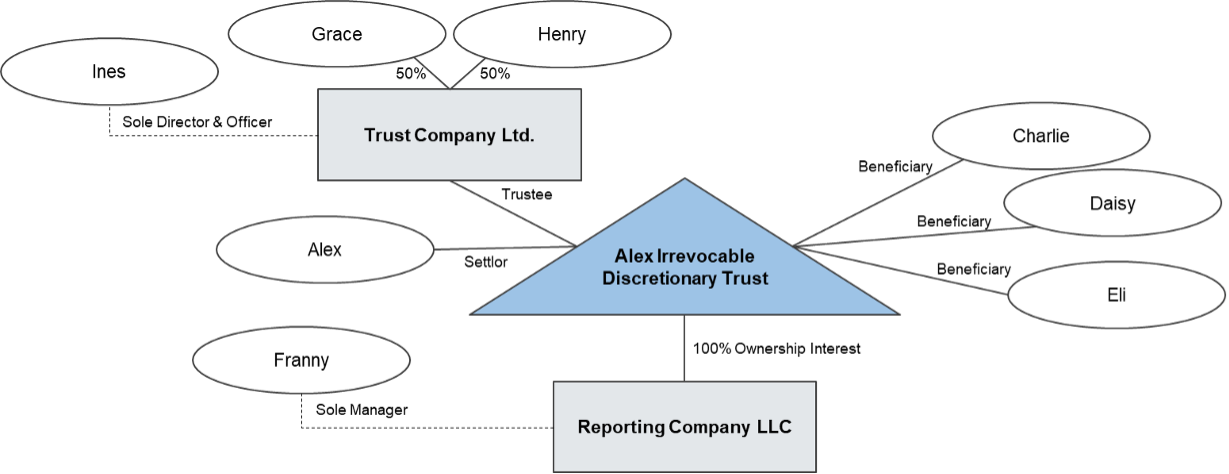

Example 6 – Corporate Trustee. Returning to the initial irrevocable discretionary trust example, assume that the trustee is an entity, rather than an individual:

Because the trustee of the Alex Irrevocable Discretionary Trust is an entity, Reporting Company LLC must look through Trust Company Ltd. to determine the LLC’s beneficial owners. In April 2024, FinCEN issued guidance on how to look through a corporate trustee. According to FinCEN’s guidance, a reporting company should:

- Determine whether any of the corporate trustee’s individual beneficial owners indirectly own or control at least 25 percent of the ownership interests of the reporting company through such person’s ownership interests in the corporate trustee; and

- Consider whether any owners of (or individuals employed or engaged by) the corporate trustee exercise substantial control over the reporting company.[27]

Here, Grace and Henry should each be attributed with ownership or control of 50% of Reporting Company LLC. This determination is dictated by the following example provided by FinCEN in its frequently asked questions:

“For example, if an individual owns 60 percent of the corporate trustee of a trust, and that trust holds 50 percent of a reporting company’s ownership interests, then the individual owns or controls 30 percent (60 percent × 50 percent = 30 percent) of the reporting company’s ownership interests and is therefore a beneficial owner of the reporting company.”[28]

In accordance with this guidance, both Grace and Henry should be considered beneficial owners of Reporting Company LLC.

Ines should also likely be attributed with ownership of 100% of Reporting Company LLC, assuming that she has authority that amounts to “indirect substantial control” over Reporting Company LLC. Indirect substantial control could include, for example, the power to remove and replace the manager of Reporting Company LLC, or exercise substantial influence over important company decisions of Reporting Company LLC. Here, Trust Company Ltd. should be deemed to have substantial control over Reporting Company LLC because the trustee of Alex Irrevocable Trust owns all of the ownership interests and voting power of Reporting Company LLC.[29] Trust Company Ltd., thus, has the power to replace the manager of the LLC, and may also have the power to exercise substantial influence over important company decisions for the LLC. Given Ines’s role as sole director and officer of Trust Company Ltd., she should have the power to exercise the corporate trustee’s substantial control over Reporting Company LLC. Accordingly, Ines should be considered a beneficial owner of Reporting Company LLC.

Finally, while the use of a corporate trustee may complicate the CTA analysis, use of a licensed trust company (including a regulated private trust company) could potentially ease the CTA compliance burdens for entities wholly-owned by the trust. As discussed by other practitioners, if a licensed trust company or regulated trustee falls within the CTA’s bank exemption (which should typically be the case), entities wholly-owned by the trust may be able to take advantage of the CTA’s subsidiary exemption, thereby avoiding reporting company status.[30] While such a position may be possible, FinCEN has yet to issue direct guidance on the subject. It remains unclear whether such a position will ultimately be successful.

Conclusion

As illustrated by the above examples, advisors may find it challenging to apply the CTA to a reporting company owned by a trust because many unresolved issues remain unresolved or unclairied by FinCEN and the CTA. Hopefully, future guidance will resolve these issues to avoid having reporting companies spend time and money to try to address the potential uncertainty. Additionally, reporting companies may face potential penalty exposure. Civil and criminal penalties may apply to willful CTA reporting violations (including failing to file or providing false beneficial ownership information). Penalties may apply to reporting companies as well as to responsible individuals and other entities. However, penalties should not apply to a reporting company that acts based on a reasonable interpretation of the law, given that penalties only apply to willful reporting violations. Notably, FinCEN has stated that it “does not expect that an inadvertent mistake by a reporting company acting in good faith after diligent inquiry would constitute a willfully false or fraudulent violation.” [31] The reach of the CTA’s penalty provisions has not yet been tested or resolved, however. Accordingly, a conservative approach may be advisable in most cases.

* * * * *

Christina S. Hammervold is senior counsel in the international trust and estate planning practice of Loeb & Loeb LLP in Chicago. Christina is an international tax and trust lawyer with significant experience counseling clients on a wide range of U.S. and cross-border tax planning matters. She has extensive experience with a broad array of global family structures and prides herself on delivering efficient, strategic, and results-oriented solutions for her clients. Christina advises private clients on cross-border planning and restructuring; pre-immigration; expatriation; cross-border income, gift, and estate tax matters; reporting requirements under the CTA; and tax regularization using IRS amnesty and disclosure programs (such as the Streamlined Filing Compliance Procedures).

[1] FinCEN is a bureau of the U.S. Department of the Treasury.

[2] See generally 31 U.S.C. § 5336.

[3] In addition to providing information about itself and its beneficial owners, a reporting company created or registered in 2024 or later must provide information about its company applicants. 31 C.F.R. § 1010.380(b)(1)(ii), (b)(2)(iv). This article does not address how to determine or report company applicants, as such issues generally are not affected by use of a trust within an entity’s ownership structure.

[4] See generally 31 C.F.R. § 1010.380.

[5] 31 C.F.R. § 1010.380(a), (c)(1).

[6] 31 C.F.R. § 1010.380(c)(1)(i).

[7] 31 C.F.R. § 1010.380(c)(1)(ii).

[8] Notably, the CTA requires a report to be submitted to Congress within two years of the effective date of final regulations regarding the wisdom of requiring beneficial ownership information for trusts. William M. (Mac) Thornberry National Defense Authorization Act for Fiscal Year 2021, Pub. L. No. 116-283, § 6502(d), 134 Stat. 3388, 4627-28. The report must evaluate whether the lack of beneficial ownership information for U.S. trusts “has elicited international criticism.” Thus, it is entirely possible that trusts may become directly subject to the CTA in the near future.

[9] 31 C.F.R. § 1010.380(c)(2).

[10] 31 C.F.R. § 1010.380(d).

[11] 31 C.F.R. § 1010.380(d)(1)(i).

[12] See FinCEN, Beneficial Ownership Information: Frequently Asked Questions, Question D.15, https://www.fincen.gov/boi-faqs#D_15 (last accessed . . . ).

[13] See FinCEN, Beneficial Ownership Information: Frequently Asked Questions, Question D.8, https://www.fincen.gov/boi-faqs#D_8 (last accessed . . . ).

[14] 31 CFR § 1010.380(d)(3).

[15] 31 C.F.R. § 1010.380(a)(2).

[16] See 31 C.F.R. § 1010.380(d)(1)(ii) (“An individual may directly or indirectly, including as a trustee of a trust or similar arrangement, exercise substantial control over a reporting company through: . . . (B) Ownership or control of a majority of the voting power or voting rights of the reporting company . . . .”); see also FinCEN, Small Entity Compliance Guide: Beneficial Ownership Information Reporting Requirements § 2.3, ver. 1.1 (December 2023) (“a trustee of a trust or similar arrangement may exercise substantial control over a reporting company”).

[17] Given current FinCEN guidance, it may be possible to read this category more narrowly, as only applying when a trustee “has the authority to dispose of trust assets.” See FinCEN, Beneficial Ownership Information: Frequently Asked Questions, Question D.15, https://www.fincen.gov/boi-faqs#D_15 (last accessed . . . ). However, the conservative position is to treat all trustees (even those without authority to dispose of trust assets) as falling within this category.

[18] 31 C.F.R. § 1010.380(d)(2)(ii)(C).

[19] See Beneficial Ownership Information Reporting Requirements, 87 Fed. Reg. 59498, 59532 (Sept. 30, 2022).

[20] See Beneficial Ownership Information Reporting Requirements, 87 Fed. Reg. 59498, 59532 (Sept. 30, 2022) (“One consequence of this—to confirm the reading that one comment suggested was possible and requested clarification on—is that, depending on the specifics of the trust arrangement, the ownership interests held in trust could be considered simultaneously as owned or controlled by multiple parties in a trust arrangement.”).

[21] Reporting companies generally have to file an updated beneficial ownership information report within 30 days of the relevant change. 31 C.F.R. § 1010.380(a)(2).

[22] In relevant part, FinCEN states the following in the preamble of the final CTA beneficial ownership information reporting regulations:

“To provide clarity, FinCEN has sought to identify specific scenarios in which individuals can be considered to own or control ownership interests of a reporting company held in trust. FinCEN has also made clear that those are specific examples of the more general principle, stated in the introductory text in (d)(2)(ii), that an individual ‘may directly or indirectly own or control an ownership interest of a reporting company through any contract, arrangement, understanding, relationship, or otherwise.’ As one commenter noted, however, trusts arrangements can vary significantly in form, so the examples in the final rule do not address all applications of the general principle.”

Beneficial Ownership Information Reporting Requirements, 87 Fed. Reg. 59498, 59532 (Sept. 30, 2022).

[23] 31 C.F.R. § 1010.380(d)(1)(ii).

[24] 31 C.F.R. § 1010.380(d)(3)(ii).

[25] See FinCEN, Beneficial Ownership Information: Frequently Asked Questions, Question D.15, https://www.fincen.gov/boi-faqs#D_15 (last accessed . . . ).

[26] FinCEN seemingly gives weight to the ownership of legal title in its frequently asked questions. See FinCEN, Beneficial Ownership Information: Frequently Asked Questions, Question D.15, https://www.fincen.gov/boi-faqs#D_15 (last accessed . . . ) (“For instance, the trustee of a trust may be a beneficial owner of a reporting company either by exercising substantial control over the reporting company, or by owning or controlling at least 25 percent of the ownership interests in that company through a trust or similar arrangement.” (emphasis added)).

[27] See FinCEN, Beneficial Ownership Information: Frequently Asked Questions, Question D.16, https://www.fincen.gov/boi-faqs#D_16 (last accessed . . . ).

[28] See FinCEN, Beneficial Ownership Information: Frequently Asked Questions, Question D.16, https://www.fincen.gov/boi-faqs#D_16 (last accessed . . . ).

[29] See 31 C.F.R. § 1010.380(d)(1)(ii)(B).

[30] Harry T. Dao & Elise J. McGee, Unpacking CTA Disclosure Complexity With Private Trust Companies, 64 Tax Management Memo. 20 (2023).

[31] Beneficial Ownership Information Reporting Requirements, 87 Fed. Reg. 59498, 59515 (Sept. 30, 2022).